Riding on the back of his most recent “success” in the Iran War, Trump is scheduled to visit President Xi on May 13 to 15. It is interesting to preview who has what “cards” ahead of the meetings and speculate what the “asks” are from each side. This way, we can have a clear-eyed view who has the leverage, who needs the other more, and what will come out of the summit.

Since Trump’s second term, he has started or continued a range of confrontations aimed at China. These include trade, technology, energy and critical minerals, military manuveurs, financial sanctions, and Taiwan.

His military adventures in Venezuela and Iran are both explicitly targeted at choke-holding China’s energy supply.

Of course, Trump also wants to “show off” how “mighty” the US military is.

In Trump’s calculation, a direct war with a superpower Russia in Ukraine is dangerous, but a crushing defeat of a second-tier regional power Iran and a third-world weakling Venezuela would serve as solid “muscle flexing” to Beijing.

Even his “spat” with Europe over Greenland is largely driven by a desire to secure critical minerals and rare earth to become less dependent on Chinese supply chains.

One could argue that much of Trump’s foreign policies in the last 16 months have been aimed at maximizing leverage over China – the US grand national strategy to contain China since the “pivot to Asia” in 2011.

So, how did things go? Who has more “cards” when the two heads of state meet in Beijing? Who has more to ask than to bestow? And who will be “bending the knee”?

The “Scorecard”

Let’s start by reviewing where the two countries stand on each of these fronts.

Trade & Economy

Trump announced his April Fool’s Liberation Day tariff war in 2025, most pointedly targeting China.

The result? China’s economy grew by 5% to reach $20 trillion, meeting the target set by Beijing in 2024.

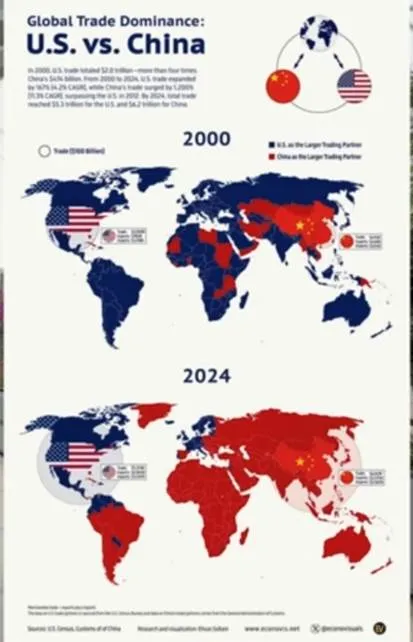

Total export grew by 6.1% to $3.8 trillion while export to the US declined by 20% to $420 billion. Export to the US represented 11% of total, down from 15% in 2024 and 19% in 2019.

In contrast, China’s export to ASEAN and EU was roughly $560 billion each, 30% higher than export to the US.

In 2025, China’s global trade surplus reached $1.2 trillion, a nearly 20% increase from 2024. It was the highest recorded trade surplus in history.

Meanwhile, the US expanded its trade deficit by 2.1% to $1.24 trillion, also a world record.

For the first four months of 2026 (January–April), China’s total exports reached $1.34 trillion, representing a year-on-year growth of 14.5%.

Its exports to the US continued to decline by over 10% in the same period.

The US now accounts for a smaller share (~9%) of China’s export than Iran’s share of China’s oil import (~13%).

In comparison with the 10% decline to the US, China’s export to ASEAN in the first four months of 2026 grew 29%. Trade with Belt and Road Countries went up 14% and up 13% with the EU.

The accelerated growth is partially thanks to unprovoked US-Israel war on Iran, which has driven up worldwide demand for green energy and EV, two industries China dominates globally.

It is unclear what “cards” Trump has when it comes to trade and economy.

Trump surely wants to secure access to rare earth and critical minerals, which China largely monopolizes.

He also wants to sell soybeans, beef, Boeing aircraft, oil and gas to China. But China can buy these from many other countries such as Brazil, the EU, and Russia.

A “chip for rare earth” deal is unlikely to work as China has not bought any Nvidia H200 chips that are “allowed” to sell to Beijing.

China clearly favors to develop its indigenous semiconductor ecosystem and completely rid itself of any US tech dependency.

A business delegation is expected to accompany Trump on his trip including the CEOs of Nvidia, Apple, Qualcomm, Exxon Mobile, Citigroup, Blackstone, Visa, and MasterCard.

His sons, Trump Junior and Eric, are joining – perhaps in hope of clinching some family deals like the hotel/resort plans with Vietnam and the Gulf countries.

It seems the business delegation is geared to sell stuff to China, who generously allows Apple and Tesla to do business in China while the US has blocked Huawei and BYD from its market and trying to block them from its vassals.

I guess “reciprocity” means something different to Trump than us normal souls. We’ll see if Beijing wants to be charitable with the Trump Organization, handing some coins to the hat held by Junior and Eric.

Technology

This is the second most visible front of the US-China confrontation.

The US regime, from Trump 1 to Biden to Trump 2, has attempted to stranglehold China’s access to advanced technologies, particularly in semiconductors and AI.

How did that go?

Huawei, the prime target of US tech embargo, has not only overcome US restrictions but is aggressively expanding in both the flagship smartphone market and the global AI chip industry.

Before the US embargo, Huawei was not even in the chip business, happily buying from Qualcomm. Now it will compete with Qualcomm and Nvidia.

Huawei’s mobile strategy is currently led by the Mate 80 and Pura 80 series, both running the native HarmonyOS 6.0 or HarmonyOS NEXT operating systems, independent from Android.

Released in late 2025, the Huawei Mate 80 Pro flagship features the new Kirin 9030 Pro chipset (a 5nm-grade processor with hardware ray tracing).

The Pura 80 Ultra is positioned as a “pioneer in imaging”, featuring a 1-inch RYYB main sensor and a world-first dual-lens switchable telephoto system.

The Pura X Mas model is a specialized passport-style foldable designed to provide a tablet-like experience for 16:9 content.

Huawei took back China smartphone market leadership – the world’s largest by far (~300 million units) – with 46.7 million units sold in 2025.

More importantly, Huawei is positioned to become a dominant player in the AI hardware space, specifically challenging Nvidia for chip design and AI software ecosystem.

Its Ascend 950 chip offers 1.56 PFLOPS compute power vs. Nvidia H200’s 1 PFLOPS and 2.5 times H200’s interconnect bandwidth for large scale cluster computing.

It is the first to feature Huawei’s self-developed High Bandwidth Memory (HBM) technology and is specifically optimized for large-scale models like DeepSeek V4.

Huawei’s CANN AI software directly competes with Nvidia’s CUDA platform.

Huawei expects its AI chip revenue to grow by at least 60% this year, reaching $12 billion due to massive orders from firms like Tencent, Alibaba, and ByteDance.

I wrote about Huawei’s full-spectrum innovation drive last year.

On the AI front, DeepSeek launched its V4 model in late April. According to MIT, the 1.6 trillion parameter V4 is a “next-generation open-source model that has reset the math of the AI industry”.

DeepSeek V4 achieves frontier-level performance in coding and STEM while costing roughly 90 to 97% less to run than OpenAI GPT-5.5 or Claude 4.7.

In Coding, V4 Pro achieved the highest score ever recorded on Codeforces (3206), surpassing all other AI models.

In Reasoning & STEM, it scores 90.1% on GPQA Diamond (graduate-level science) and 95.2% on HMMT 2026 (math). It trails slightly behind GPT-5.4.

In Recall, it features a 1 million token context window (approx. 750,000 words). In NIST CAISI evaluations, it demonstrated better factual recall than Gemini 3.1 Pro when retrieving data buried in long documents.

The defining feature of V4 is its “Compressed Sparse Attention” (CSA). This revolutionary mechanism creates a smart index of a document rather than reading every word every time.

It is the first major model natively optimized for FP4 precision on Huawei Ascend 950 clusters. This allows Chinese developers to bypass Nvidia hardware entirely.

While Anthropic Claude Opus 4.7 still holds a slight lead in “nuanced” reasoning and presentation, DeepSeek V4 Pro is priced at $1.74 per million output tokens.

This compares with the $25 and $30 per million token prices offered by Opus 4.7 and GPT-5.5, the flagship models from Anthropic and OpenAI.

V4’s pricing advantage, a result of its vastly more efficient production, has led many enterprises to use DeepSeek for “bulk work” and reserve top-tier US models only for high-stakes planning.

In the most recent Standford University HAI (human-centered artificial intelligence) study, the authoritative annual industry report concludes “the U.S.-China AI model performance gap has effectively closed”.

The report pointed out “U.S. and Chinese models have traded the lead multiple times since early 2025. In February 2025, DeepSeek-R1 briefly matched the top U.S. model, and as of March 2026 Anthropic’s top model leads by just 2.7%”.

“The U.S. still produces more top-tier AI models and higher-impact patents, while China leads in publication volume, citations, patent output, and industrial robot installations”. You can read the HAI report in full here. https://hai.stanford.edu/ai-index/2026-ai-index-report

China has pursued the opposite path from the US to develop, diffuse, and democratize AI through open-source open-weight frontier models such as DeepSeek, Qwen, Kimi, and Seedance 2.0, ByteDance’s flagship multimodal AI video generation model.

China’s open-source approach to AI development has vastly improved efficiency and reduced costs for global AI developers, making diffusion and scaling possible for those with limited funding and access to compute.

On January 12, the Financial Times reported that Microsoft president Brad Smith warned that US AI companies are being overtaken by Chinese competitors in the race for users, citing China’s low-cost open-source models as a key advantage.

Alibaba’s Qwen family of AI models have recorded 700 million downloads on the Hugging Face collaborative AI platform by end of 2025, making it the most popular open-source AI system worldwide.

Token consumption of DeepSeek models on OpenRouter between November 2024 and November 2025 topped 14 trillion, placing it first globally and surpassing the combined usage of the next four models from China’s Alibaba, Europe’s Mistral AI and US firms Meta and OpenAI.

OpenAI began with a mission of transparency in AI, a mission it abandoned in 2022 as the company began to withhold details of its technology. It should be more properly named “ClosedAI”.

The growing prowess of Qwen and DeepSeek and other Chinese models is fueling a “global diffusion” movement, wrote the HAI scholars.

“Countries around the world, but especially developing-world nations, are going to take up Chinese models as an inexpensive alternative to trying to build their own AI from scratch.”

“As a result of their technical proficiency and greater openness, Chinese models are increasingly becoming a way for developers around the world to access free code and create efficient, tunable models for various purposes.”

“The wide availability of high-performing Chinese AI models opens new pathways for organizations and individuals in less computationally resourced parts of the world to access advanced AI,” wrote Meinhardt and team, “thereby shaping global AI diffusion and cross-border technological reliance patterns.”

The authors predict the diffusion trend will sustain itself because the economic benefits outweigh continued benchmark achievements by OpenAI and the other closed frontier AI models from the US.

“With model performance converging at the frontier, AI adopters with limited resources to build advanced models themselves, especially in low- and middle-income countries, may prioritize affordable and dependable access to enable industrial upgrading and other productivity gains.”

And it’s not just the developing world. “US companies, ranging from established large tech companies to some of the most hyped AI startups, are widely adopting Chinese open-weight models,”

“The existence of open-weight Chinese models at the good-enough level may thus decrease global actors’ reliance on US companies providing models through APIs.”

US companies that have embraced China open-source AI foundational model for their AI development include AirBnB, Shopify, Pinterest, Databricks, Cognition AI, Perplexity, and Uber.

China’s open-source strength and its strategic implications are echoed by a US government study in March.

The US-China Economic and Security Review Commission published a lengthy report titled “Two Loops: How China’s Open AI Strategy Reinforces Its Industrial Dominance?” Full report here: https://www.uscc.gov/research/two-loops-how-chinas-open-ai-strategy-reinforces-its-industrial-dominance

The report highlights China has opted to go all in on an open-source approach to AI. Most Chinese labs publish model source code and weights.

They also charge far less to use high-end products than their global competitors. This has resulted in the acceleration of global uptake of Chinese AI and created a feedback loop where widespread adoption drives iteration, then further adoption.

It noted Alibaba’s Qwen models accounted for the largest model ecosystem on Hugging Face, with over 100,000 derivatives.

The report further explains China’s open AI model strategy and its manufacturing dominance are mutually reinforcing. China’s industrial base generates “interlocking innovation flywheels” across adjacent sectors.

Open models accelerate this dynamic by enabling low-cost AI deployment across factories, factories, logistics networks, and robotics—generating real world data that feeds back into model improvement.

Furthermore, the report points out that the US export controls primarily target the digital loop—restricting access to advanced chips used for frontier model training—but are not suited to addressing the physical loop of deployment-driven data creation and accumulation across China’s manufacturing base.

As open models reduce the compute required for effective deployment, China’s ability to generate proprietary industrial data at pace and scale becomes increasingly independent of access to cutting-edge hardware.

This gap in the US policy framework means that even successful controls on training compute may not prevent China from building AI advantages rooted in its physical economy.

Apart from AI large language models, China accounted for over 90% humanoid robot installations globally in 2025, driven by domestic start-ups AgiBot and Unitree Robotics.

A total of 16,000 humanoid robots were installed globally in 2025, mainly for data collection and research, as well as in the logistics, manufacturing, and automotive sectors, according to Counterpoint data.

Shanghai-based AgiBot led the market with a 30% share of installations worldwide in 2025, followed by Hangzhou-based Unitree’s 26%.

Shenzhen manufacturers UBTech Robotics and Leju Robotics ranked third and fourth, ahead of Tesla’s 4% global share with Optimus Gen 2 and Gen 2.5.

If Trump thinks he has any leverage over China through tech embargo, he clearly doesn’t understand anything about the subject – which is of course exactly the case.

Energy and critical minerals

Trump’s Iran War and attack on Venezuela are both motivated, at least partially, by a desire to chokehold China’s oil supply.

Venezuela and Iran together represent 16-17% of China’s crude import.

However, the effort has clearly backfired. While petrol price in China went up from 7.5 yuan per litre before the war to 9 yuan per litre in May (19% rise), it is far lower than the 50% hike in the US ($3.1 per gallon to $4.5).

China has not even used any of its strategic petroleum reserve, which is the world’s largest at 1.8 billion barrels compared with the US’s 400 million barrels.

The reason is the Chinese economy, though by far the world’s largest energy consumer, is far less dependent on oil & gas than the US.

China’s energy mix is completely different from the US. Coal still accounts for 50% energy need and China is self-sufficient. Renewables and low carbon sources (such as nuclear power) in China contribute a much larger portion of its energy need than the US (25% vs. 15%).

China is dependent on oil and gas for only 26% of its energy need (18% and 8% respectively) while the US is dependent on oil & gas for 72% of its energy need (36% each).

China also has the world’s most diverse oil and gas imports from nearly 50 countries including Russia, Algeria, Brazil, Iraq, Malaysia, Canada, Turkmenistan, and Nigeria.

The US needs to go to war with most of the world to block China’s energy imports.

From 2021 to 2025, China’s domestic solar power-generating capacity quadrupled, roughly equalling the entire generating capacity of the US, according to the US Council on Foreign Relations.

China’s total electricity consumption in 2025 hit 10.4 trillion kilowatt-hours (kWh), roughly 2.5 times that of the US at 4 trillion kWh.

China’s electricity capacity expansion is 9 times that of the US. China adds two Germany’s generation capacity every year.

China produces over 1/3 of the world’s electricity. Its 10.4 trillion kWh power generation exceeds the combined total of the US, EU, Russia, India and Japan.

Electricity generation and consumption are widely recognized as the best proxy for real economic activity.

The Kardashev Scale measures a civilization’s technological advancement directly proportional to the amount of energy it can harness.

This gives you a sense of the size of China’s “real economy” vs. the US.

If Trump thinks he can squeeze China on the energy front, he suffers the same delusion as the “tech chokehold”.

Instead, the Iran War has shown the world’s dependency on Chinese refined oil products such as jet fuel and fertilizers such as urea, ammonium phosphate, nitrogen-potassium, and sulphuric acid.

China is Asia Pacific’s largest jet fuel exporter and implemented a near total ban on refined oil product exports – including jet fuel, diesel, and gasoline – to secure domestic stockpile.

This has triggered a global supply crunch and a doubling of international prices. Australia and Japan are hardest hit as both are heavily reliant on Chinese jet fuel. Sydney Airport recently warned it could not guarantee fuel availability for May.

Vietnam is struggling to maintain supplies to its airlines as it imports roughly 60% jet fuel from China.

Jet fuel price doubled from $99 per barrel before the war to $195 by early May. The Spirit Airline in the US went bankrupt.

China also produces 30-40% of the world’s fertilizers, especially the critical ammonium phosphate and urea.

When China implemented a sweeping tightening of fertilizer export to prioritize its own domestic food security, farmers in the US, India, and numerous other countries faced short supply, price hikes, and potentially massive output loss.

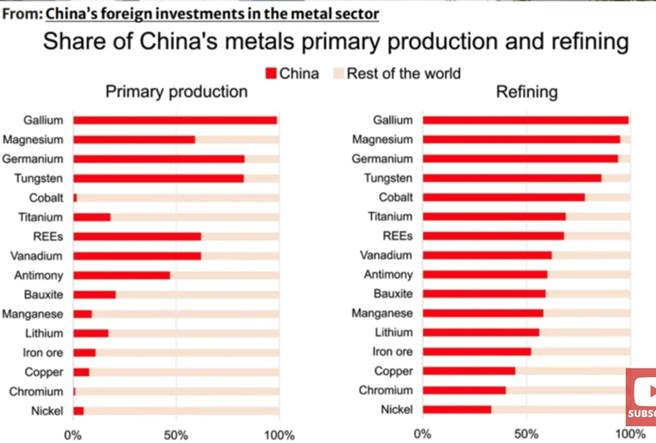

On the other hand, China continues to dominate the world’s supply of rare earth and critical minerals such as gallium, tungsten, lithium, cobalt, and graphite.

Despite US and the West’s effort to diversify, China’s lead in refining technology, know-how, existing capacity and cost advantages are simply too great to overcome for decades.

Trump thought his attacks on Venezuela and Iran would put China’s energy supply in a squeeze.

I wonder who will be begging whom in Beijing for energy and critical minerals.

Military overmatch

I wrote extensively about the “underwhelming” performance of the US military in its joint war with Israel against Iran.

So instead of going to details to make the point that the US has zero leverage militarily over China, I’ll just quickly highlight its disastrous performance in front of the world in the last 2 months.

By all intents and purposes, the US has lost the war to Iran –

– The US has achieved none of its stated “objectives” for the war;

– Iran now controls the Strait of Hormuz and effectively controls the Middle East energy supply;

– Iran has pummelled Israel and every US base in the Gulf, destroying tens of billions worth US assets.

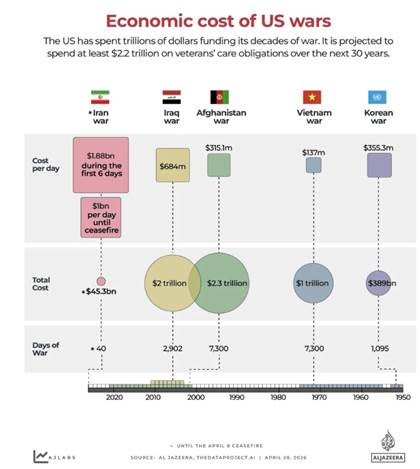

The Iran War cost the US between $25 billion (according to the low-ball Pentagon estimate to Congress) and $50 billion (according to CSIS, CNN, Fortune).

The CSIS estimate includes direct expenditure of missiles and ammunitions worth $25 to 35 billion and lost assets (radars, jets, mil bases) as well as logistical costs estimated at $15 to 25 billion.

There is no reliable estimate of the cost and time needed to repair the US bases in the Gulf, if the Gulf monarchs allow the US to rebuild (and thus making themselves potential future targets).

The US has embarrassed itself and shocked the world with the incredible depletion of its weapons stockpile and loss of critical assets to Iran’s low-cost drones and short-range missiles:

– 50% of THAAD and Patriot air defense interceptors

– 25-40% of Tomahawk and JASSM-ER attack missiles. CSIS reported the US fired Tomahawk missiles in a month that are 10 times its annual production rate

– 80-100% PrSM new long-range missiles

– 5 to 7 high-value radars worth $3-4 billion

– Numerous aircrafts including 5 F-15EX (over $100 mil each), 1 E-3 Sentry (worth $700-800 mil), at least 7 KC-135 Stratotanker, at least 2 A-10 Warthog, 2 MC-130J air lifter (over $110 mil each), 1 MQ-4 Triton (worth $250 mil), at least 24 MQ-9 Reaper

– Damage to all military bases in the Gulf region, forcing the US military personnel to “work remotely” from civilian buildings and Europe

According to CSIS and other estimates, the US will need 4 to 8 years to replenish and replace the lost military assets and munitions.

Below graph shows the cost of the Iran War compared with the many other US military adventures in the past 60 years.

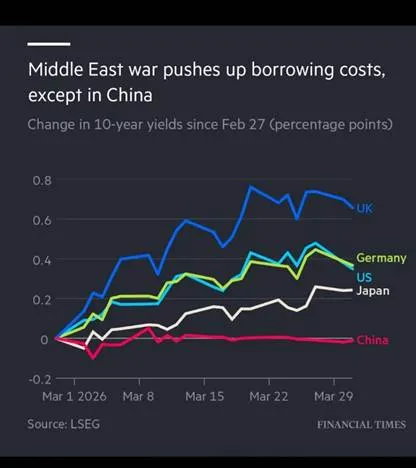

Besides the astronomical war cost, the US is facing an even bigger problem – escalating cost of capital to finance its $39 trillion national debt.

The graph below shows the borrowing cost of major economies after the war. If Trump doesn’t understand this, he can get Scott Bessent to explain.

Trump probably thought he would come to Beijing a “victor” when he launched the joint war with Israel on Iran.

He is now going decidedly a “loser”. However he spins his defeat into a glorious “victory” to his dumb domestic audience, reality won’t change from chicken shit to chicken salad.

Financial Sanctions

The US Treasury put 5 Chinese oil refiners on its sanction list late April. The pretext was these companies bought “sanctioned” oil from Iran.

Even the blind can see the intent is to give Trump some leverage for the upcoming meeting with President Xi.

Rather than its usual diplomatic protest, Beijing invoked its 2021 Blocking Rules, for the first time, to legally prohibit any firms from complying with the US measure.

Chinese Foreign Ministry and Ministry of Commerce have “categorically rejected” the sanctions, describing them as –

– Illegal and unilateral: Beijing maintains any sanctions without UN Security Council endorsement as illegitimate under international law;

– Malicious extrajudicial application of US domestic law: Beijing doesn’t recognize the legality of US laws over Chinese firms conducing business with a third-party country

On May 2, 2026, MOFCOM issued a groundbreaking Prohibition Order (Announcement No. 21) that:

- Mandates Non-Compliance: It explicitly orders Chinese citizens and companies “not to recognize, not to enforce, and not to comply” with U.S. sanctions on five major domestic oil refineries

- Creates a “Compliance Catch-22”: Companies operating in both markets, including foreign firms, now face an “Odysseus dilemma”: complying with US sanctions violates Chinese law, while ignoring them could result in being cut off from the US financial system

Beijing’s approach clearly sends a message that China’s energy security and protection of its own firms are non-negotiable red lines before the summit meeting.

Beijing is letting the US know it has had enough of the illegal and unilateral US sanction regime that has been imposed on one third of the global population.

If necessary, China is ready to take the bottom out of the US global financial architecture including the SWIFT and the Bank of International Settlement (BIS) systems.

Taiwan

For many in the US, this renegade island 130 kilometers from the Chinese mainland is Trump’s last “card”.

In reality, Taiwan is a “poison pill”. The US will be defeated roundly if it goes to war with China over Taiwan. If it doesn’t, Washington will lose all credibility to its vassals since the US political class has been making noises of “protecting Taiwan” for decades.

There are lots of opinions both in China and outside during the Iran War that time was perfect for China to take back Taiwan as the US is tied down in another distant war of choice.

On the surface, the argument makes a lot of sense –

– The US certainly has no ability to fight two major wars 7,000 kilometers apart;

– Taking Taiwan and the semiconductor industry on the island will instantly pop the AI bubble which is single-handedly propping up the US economy and equity market;

– A two-front defeat will rid the world of US hegemony once and for all, freeing the world from its “bully par excellence”

It’s hard to imagine that strategists in Beijing haven’t put things together and reached the same conclusion.

The fact Beijing has decided not to take advantage of the window of opportunity is a clear signal that the Taiwan issue is not dependent on the US position, one way or the other.

Whatever the US decides to do – interfere or not – simply won’t change the outcome if China decides to take back Taiwan militarily.

With the passage of time, the US becomes an even less relevant factor in Beijing’s calculations.

Beijing still prioritizes peaceful reunification even if it means a longer wait and potentially a bloodier fight if peaceful reunification becomes impossible.

This is so simply because Beijing is confident that China will prevail.

The bottom line is Trump has no “Taiwan card” to play.

What all this means

Trump will come to Beijing with very little to offer and a long wish list:

– Trump wants China to sell US rare earth and critical minerals;

– He wants to sell soybeans, beef, aircraft, oil & gas, and probably semiconductors to China;

– Trump likely hopes President Xi will exert influence over Iran and broker a face-saving end for his ill-conceived war

He may get some of his wishes. President Xi wants a stable China-US relationship but won’t accept anything that counters China’s national interests.

There might be some “tactical deals” from the summit. But Beijing knows not to trust Trump or Washington.

After all, Trump launched two sneak attacks on Iran within a year under the pretence of “negotiations”. He is not a good-faith actor and cannot be trusted, period.

The US government has a long history of going back on its own words, starting with the Peace Pipe deals with the Native Americans (the Calumet Ceremonies).

For indigenous Native Americans, smoking the pipe was a solemn act of “truth-telling.” To smoke together was to invoke the Creator as a witness to an agreement.

Breaking a promise made over a pipe was considered a profound spiritual violation.

However, the colonial negotiators from the US government repeatedly participated in these ceremonies to gain the trust of Indigenous leaders, only to later violate the terms of the treaties they had just “sanctified”, leading to tragedies like the “Trail of Tears” for the native peoples.

In other cases, the ceremony was used by the US colonizers as a stalling tactic or a way to lower the other side’s guard while military maneuvers were being planned elsewhere.

Historically, the US government has repeatedly engaged in offering a false “peace pipe” as a distraction or a false front of friendship while secretly preparing an ambush.

Beijing is keen student of history and has long learned to judge a foe by their acts, not their worthless words.

Trump has no “cards” to play in Beijing. I expect him to enjoy the food and the pomp but in the end, the fraud will return home empty-handed.