March 10, 2026 – The country’s oil production is far from covering the shortfall caused by the closure of the Strait of Hormuz.

One of the most widespread geopolitical theories in recent weeks is the exaggeration of a supposed masterstroke by Donald Trump in Venezuela to seize its oil and thus be able to wage war against Iran. While this has been repeated many times by experts in “geopolitics” and enthusiasts of international relations, the reality is quite far removed from this thesis, which presents the intervention in Venezuela as a mere arithmetic useful for Trump’s calculations. And one of those responsible for this situation is the US president himself.

Venezuela produces 1 million barrels per day compared to the 20 million barrels that pass through the Strait of Hormuz; only 5% of what crosses this maritime corridor, according to the U.S. Energy Information Administration (EIA). Despite this, the Trump Administration continues to refuse to use its strategic reserves to lower oil prices, reserves estimated at 415 million barrels. According to Karoline Leavitt, White House Press Secretary, “The Trump Administration’s policies have led to the highest U.S. oil production in history, with even more oil coming from our new market and agreements with Venezuela.”

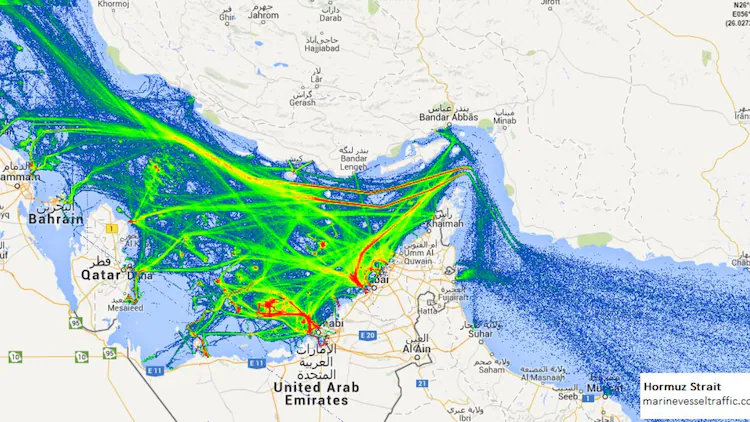

This masks a rather elusive mathematical problem for the White House: in the most recent agreements with Venezuela alone, trading companies approved by Washington sold nearly 100 million barrels of Venezuelan crude between February and January. This represents a total of five days’ worth of flow through the Strait of Hormuz. This demonstrates how difficult it would be to fulfill the maxim that Venezuelan oil would bolster Trump’s domestic position with an abundant supply capable of withstanding the shock of a Hormuz closure and a drop in oil production from countries like Iran, Qatar, Saudi Arabia, and the United Arab Emirates. To put this into perspective, approximately 5.5 million barrels per day flow through the Strait from Saudi Arabia, about 3.5 million from Iraq, between 2 and 2.5 million barrels per day from Iran, between 2 and 3 million from the United Arab Emirates, and between 2 and 3 million from Kuwait.

Eighty-four percent of the crude oil passing through the Strait of Hormuz is destined for Asian markets; Japan relies on imports for 75% of its needs, South Korea for 70%, India for 60%, and China for 40%,

according to a report by expert Adrián Arias . Meanwhile, the United States imports only 0.5 million barrels per day from this region, barely 2% of its consumption, according to

a report by the Institute for Energy Research . For U.S. Secretary of the Interior Doug Burgum: “Washington has no reason to worry. Others in the world do.”

However, the problem for the White House is not the crude oil supply, but the soaring prices caused by the reduction in oil shipments through the Strait. In the first hours of the US operation Epic Fury, tanker traffic through the Strait of Hormuz fell by 70%. Iran will burn any oil tanker that passes through the Strait of Hormuz, threatened General Amir Ali Jabari, advisor to the country’s top military commander. “We will not allow a single drop of oil to leave the region. The price of oil could reach $200,” he stated.

Alternative routes are dramatically insufficient. Saudi Aramco’s East-West pipeline (Abqaiq-Yanbu) has a capacity of between 5 and 7 million barrels per day, Abu Dhabi’s ADCOP (Habshan-Fujairah) reaches 1.5 million, and the Iraqi-Saudi IPSA has 1.65 million, although it is in reserve. The actual available surplus capacity is only between 2.6 and 3.5 million barrels per day, according to the EIA , leaving between 14 and 17 million barrels per day structurally tied to maritime transit through the Strait. Iraq, Kuwait, and Qatar lack any viable alternative. This is why financial analysis firms like Wood Mackenzie and UBS project scenarios where oil prices per barrel range from $100 to $120 if the flow through the Strait of Hormuz is completely shut down.

This entire scenario highlights the political vulnerability of the White House should gas prices rise in the United States. Such a shortage would be difficult to cover with Venezuelan oil; a type of oil that supplies the Gulf Coast refineries, which are equipped to process heavy and extra-heavy crude. Venezuelan Merey crude, which comes from the Orinoco Belt and is upgraded with diluents, has a lower sulfur content than Iraq’s light Basra and Saudi medium crude, according to oil expert Einstein Millan Arcia . In theory, it would be ideal for making up for the shortfall. For now, thanks to the oil agreements between Donald Trump and Narendra Moodi, refineries like Reliance have the option of importing Venezuelan crude to replace some of the barrels they receive from the Strait of Hormuz.

One of the reasons Venezuela cannot be Donald Trump’s pawn in the oil markets is its own actions. According to the Venezuelan Anti-Blockade Observatory, the sanctions and oil embargo imposed by his first administration coincided with a collapse in oil production from over two million to nearly 200,000 barrels per day. Only a few years ago was the state-owned PDVSA able to recover its production through Productive Participation Agreements, a transfer of oil assets to private entities, reaching almost one million barrels per day this year.

The sanctions, coupled with poor PDVSA management policies, necessitate a $100 billion investment, according to Millan Arcia and other experts, to rebuild the country’s oil infrastructure. With this massive injection of funds, the best-case scenario would be that in the coming years, Venezuela would reach a maximum production of four million barrels per day, something that seems entirely unattainable. Even if this were the case, it would still fall far short of the Hormuz refinery’s flow rates.

The geopolitical advantage of controlling Venezuela, however, is not immediate: the country boasts reserves of 270 billion barrels of heavy and extra-heavy crude, 30 billion barrels of medium, light, and condensate crude, and enormous gas deposits of 200 trillion cubic feet, which, converted to crude oil equivalent, represent a monumental production capacity, according to Millan Arcia, former PDVSA manager. “There is a huge difference between a production cost for a company like Exxon of $30 per barrel for an asset with a limited lifespan like those in Guyana—less than 10 or 15 years—and assets like Venezuela, which can have production costs close to $10 to $15 per barrel and a lifespan of more than 20 years.”

If Trump’s energy strategy were to succeed, and all that oil potential were developed, the United States would have significant “energy security” to initiate a long-term global war and support its allies, as happened in World War II. Also, if regime change were to occur in Iran, Washington could more easily drive Russian oil out of the market by offering Iranian and Venezuelan barrels instead.

But all of those are assumptions, like the theory that Trump “took over Venezuela to launch a major war against Iran.”